{kind=link}

With the release of the draft IRS forms for reporting advance premium tax credits and reconciliation with the household MAGI, health insurance agents might be called upon to know another part of the ACA, the dreaded tax forms. The variety of reporting statements individuals and families may receive from employers and the exchanges will require explanation beyond what IRS guidance and instruction will provide.

These are draft forms released without any instructions or guidance. The IRS may subsequently change the format of the forms. The following comments should not be taken as instructions but a quick glance at how the tax forms might be used. The draft forms can be downloaded at the end of the post.

What’s a SLCSP?

The Exchange Statement,f1095a,looks like it will be a straight forward reporting document on how much tax credit was advanced on behalf of the household to the chosen health plan month by month. What will be confusing to the recipient is the reporting of the Second Lowest Cost Silver Plan (SLCSP) on the Exchange Statement and why it needs to be transferred to Form 8962 the Tax Premium Credit reconciliation form. The premium of the SLCSP in the household’s region is the benchmark on which the monthly Advance Premium Tax Credit (APTC) is based. If the family moves from one pricing region to another, the SLCSP will change and in turn affect their monthly APTC.

Households may receive multiple Form 1095a Exchange Statements

A family may receive multiple statements if they move out-of-state and were also covered by an employer based plan. For example, a family may have been covered by the federal exchange when the lived in Idaho, then enrolled in the California state based exchange and later in the year transitioned to an employer health plan. This family would receive a Federal Exchange Statement, a California Exchange Statement and finally an employer form showing they had credible coverage through a group plan.

{kind=link}

The federal or state exchange will report the amount of tax credit advanced each month on behalf of the household with an Exchange Statement 1095a.

Don’t forget income from your child’s part-time job

All of these various IRS statements and forms which must reach the household by January 31st are then used to complete the Tax Premium Credit reconciliation form of 8962. Another point of clarification for families is that on line 2b of 8962 they need to report the income of other dependents in the family plan. For example, children who have taxable income from part-time jobs need to have thatincluded for an accurate determination of the household Modified Adjusted Gross Income (MAGI).

401% of FPL loses APTC

It’s possible that children on their parent’s health plan who secured part-time jobs during the year will push the household MAGI over 400% of the Federal Poverty Line (FPL). On line6 of 8962, the primary applicant of the ACA Tax credits must determine if the calculated MAGI falls below or exceeds that 400% threshold. If it exceeds 400% the family may have to repay all the APTC they received during the year.

What is affordable?

The next part of 8962 is essentially what the federal and state exchanges do when they crunch the numbers from a household’s application to determine the monthly APTC. With a MAGI of under 400% of the FPL, the tax filer must then determine the “applicable figure” for their income. While there is no definition of “applicable figure” on the form, it looks to be the affordability percentage the ACA concluded was the maximum amount a household should spend on their health insurance based on their MAGI. For instance, a single individual making $26,000 or between 200% and 250% of the FPL is expected to pay 6.3% of his or her MAGI on health insurance.

A cap on the APTC

The difference between the SLCSP and the amount the household is expected to shoulder, as an affordable health insurance premium, is the potential maximum APTC. Of course, the annual tax credit can’t be larger than the actual annual premium for the household if the premium is less than the total of the SLCSP. This might happen if the family chooses a Bronze plan and the monthly APTC covers the premium amount of the health plan.

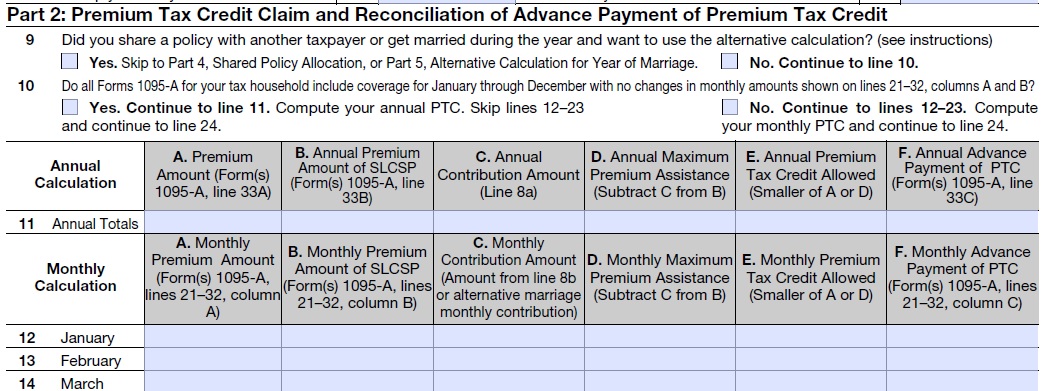

Crunching the numbers

For individuals and householdswho have had the same health plan and APTC throughout the year will they complete the tax premium calculation on Line 11 of 8962. From the Exchange 1095a Statement and calculationfrom Part 1 of 8962the family will enter:

- Annual premium of their health plan

- Annual premium of the Second lowest Cost Silver Plan from their region

- Annual affordable premium amount they are expected to pay from Line 8a of 8962

- The annual maximum premium assistance, B minus C

- The maximum APTC allowed, the lower of either A or D

- Total amount of tax credit advanced from the exchange

{kind=link}

IRS Form 8965 will walk ACA tax credits recipients through calculating any excess advance tax credits they must repay.

Limiting repayment

The household will thenreport the difference between E, the maximum APTC allowed, and F, the total APTC sent to the chosen health plan, Lines 24 – 27. If the family was entitled to more APTC than they received, they can claim a credit on their 1040 tax return. Similarly, if they received excess APTC for their MAGI, they will report that liability on their federal tax return. Lines 27 and 28 determine if there is a limit to the excess APTC that has to be repaid. While this is not on the form, the table will be in the instructions and can be found in the IRS Final Regulations that can be downloaded at the end of the post.

Numerous household changes complicates calculations

Either the additional credit or the excess repayment will be reported on the front page of the updated 1040 federal tax return forms. The difficulty of the calculation for the tax credit with 8962 will be increased if the household has numerous changes from moving to a different state, region, added household members or reported changes to income. All of those changes recalculated the APTC and will need to be entered on a month by month basis on 8962.

The marriage knot

For tax payers who either shared a health plan or got married during the year the IRS offers alternative calculations for determining the health insurance premium tax credit. The draft forms don’t provide any real explanation as the instructions for these forms haven’t been released. However, the IRS Final Regulations on the Health Care Tax Credit does outline how these alternative calculations can be made. The alternative calculations may be so daunting for the average human to figure out that a tax program or tax preparer may be the best course of action for families with this situation.

Agents with answers

As agents, we are always told never to give tax advice. I live by that rule. However, there is no prohibition against knowing what resources are necessary to fill out a complicated tax form. The tax preparation software and the in-person tax preparers will have all the instructions to help families through the process. But agents can be a valuable resource on what the terms such as SLCSP mean and why they are important for their clients.

Draft Instructions Form 8962 (0.4 MiB) F1094b--dft Transmittal (95 KiB) F1094c--dft Employer Sponsored (0.1 MiB) F1095a--dft Exchange Statement (0.1 MiB) F1095b--dft Health Coverage (0.2 MiB) F1095c--dft Employer (0.2 MiB) F8962--dft IFP APTC Calc (0.2 MiB) F8965--dft Exemption (0.1 MiB)

IRS final regulations on ACA Advance Premium Tax Credit definitions, eligibility, calculations, employer sponsored plans, repayment of excess APTC and calculation of the APTC under mid-year household changes such as birth of child, marriage or loss of dependent.

| Category: | IRS |

| Date: | May 18, 2014 |